Quick Answer

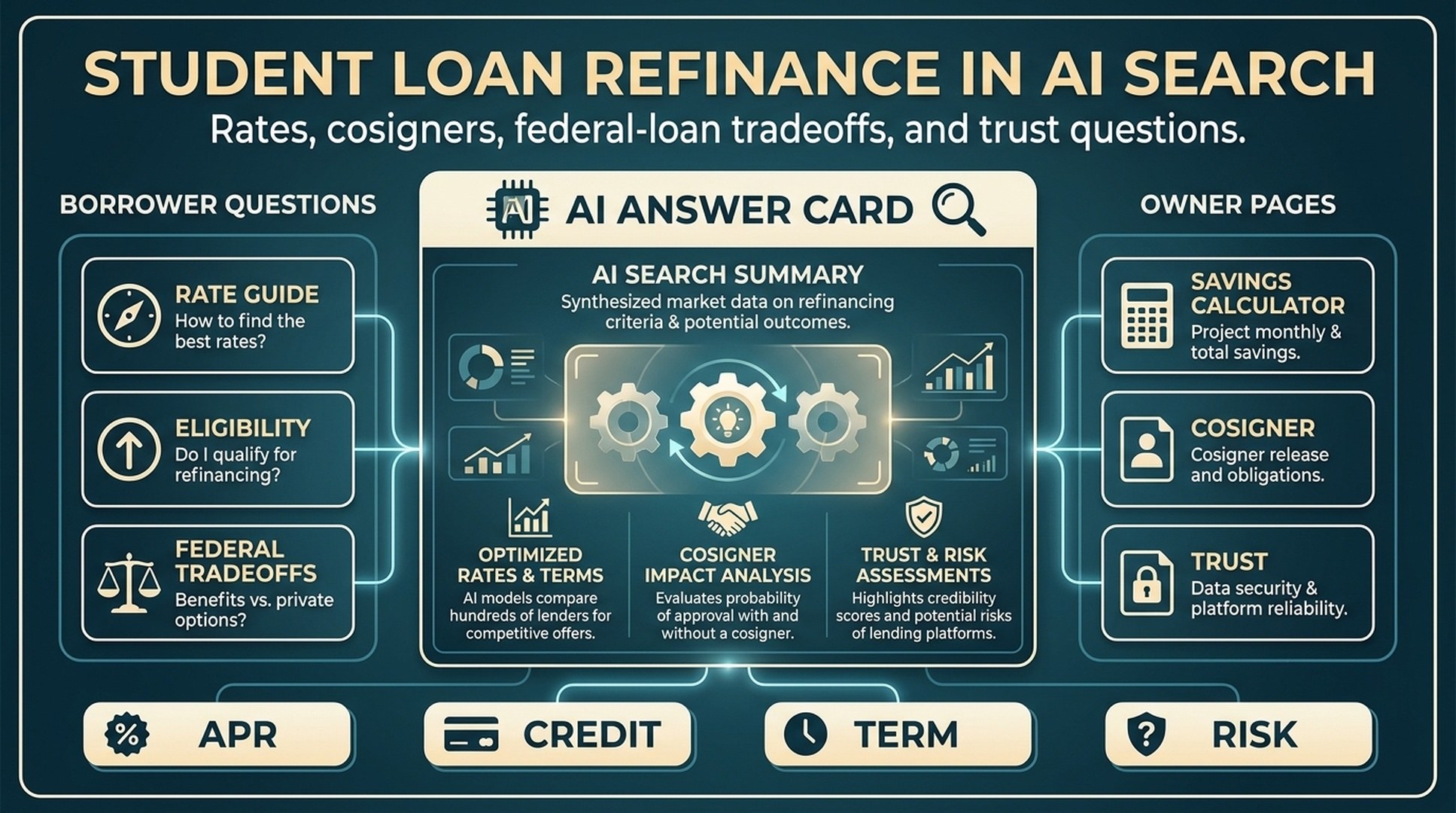

Student loan refinance GEO should start with the questions borrowers ask before they trust a lender: "Will I get a lower rate?", "Do I need a cosigner?", "What credit score qualifies?", "Should I refinance federal loans?", "How much will I save?", and "Which lender is safe to apply with?"

For refinance lenders, fintech marketplaces, credit unions, banks, and loan comparison brands, the best AI Search content usually maps borrower questions to six owner assets:

| Borrower question | Best owner asset | Proof AI systems can extract |

|---|---|---|

| Can I lower my rate? | Rate eligibility guide | APR range, fixed vs variable explanation, soft-check workflow |

| Do I qualify? | Refinance requirements page | Credit, income, degree, loan type, debt-to-income factors |

| Should I refinance federal loans? | Federal-loan tradeoff guide | Benefit-loss caveats, IDR and forgiveness references, risk notes |

| Do I need a cosigner? | Cosigner and release guide | Approval factors, release criteria, borrower responsibilities |

| How much can I save? | Savings calculator page | Assumptions, term comparison, total interest and payment tradeoffs |

| Is this lender trustworthy? | Lender trust page | Licenses, disclosures, reviews, support, privacy, servicing details |

The goal is not to publish 100 small keyword pages. The goal is to build a rate-and-risk library that helps AI systems summarize your terms accurately and helps borrowers avoid decisions they do not understand.

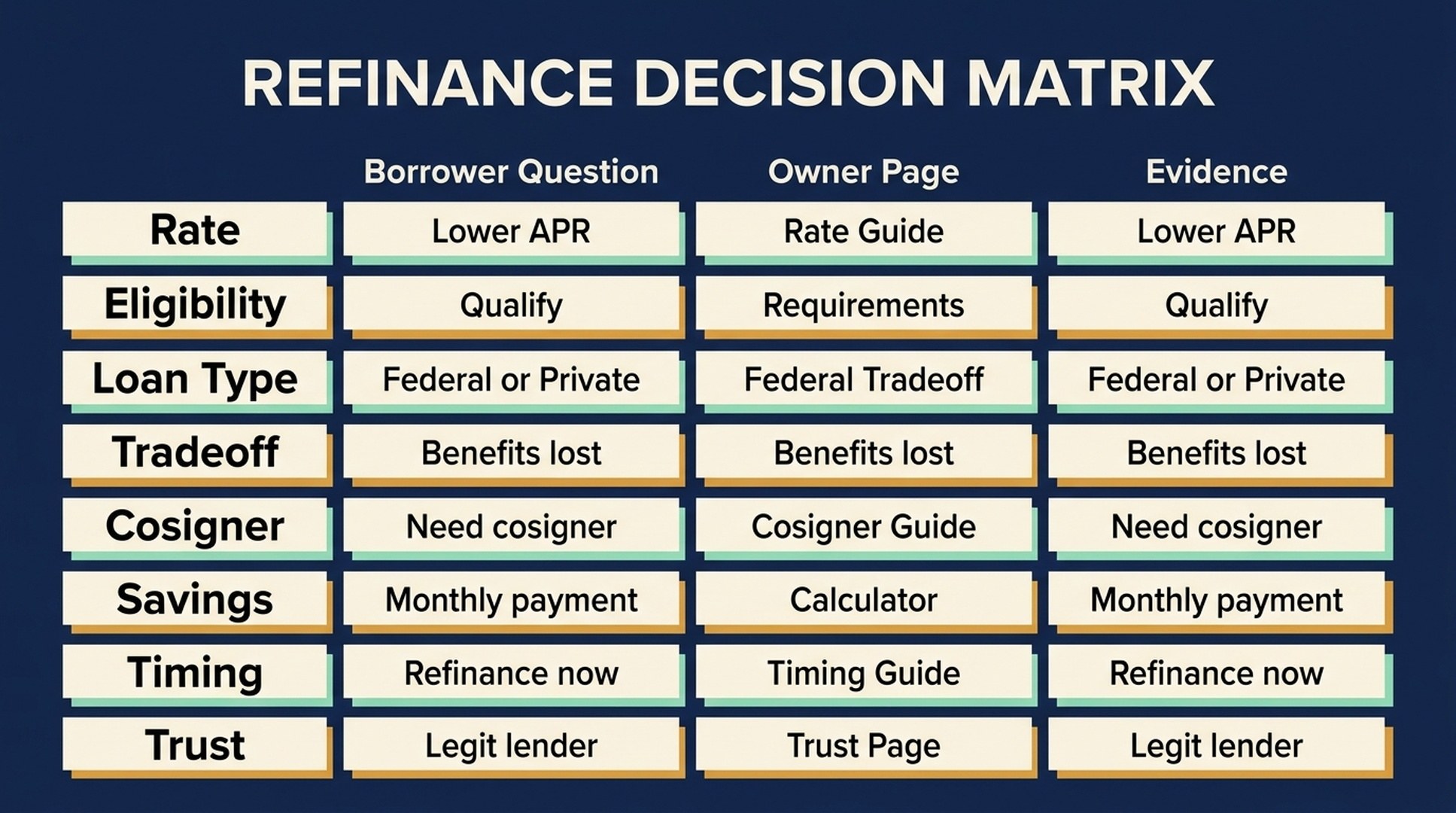

The Refinance Decision Matrix

Student loan refinance is not a single-intent keyword. It is a decision matrix with money, eligibility, timing, and risk all moving at once.

| Decision layer | What the borrower needs to know | Content job |

|---|---|---|

| Rate | What rate might I qualify for? | Explain fixed APR, variable APR, soft credit checks, credit tiers, and rate estimates |

| Eligibility | Can I get approved? | Explain credit score, income, employment, degree, school, loan balance, and DTI factors |

| Loan type | Are these federal or private loans? | Explain the difference between refinancing and federal consolidation |

| Tradeoff | What benefits might I lose? | Explain federal protections, repayment plans, deferment, forbearance, and forgiveness considerations |

| Cosigner | Do I need one? | Explain cosigner approval, responsibility, and release conditions |

| Savings | Will refinancing actually help? | Show payment, term, interest, and cash-flow scenarios |

| Timing | Should I refinance now or later? | Explain rate environment, credit improvement, job changes, and payoff stage |

| Trust | Which lender should I choose? | Show transparent disclosures, fees, servicing, reviews, and support policies |

Auspia's recommendation: write refinance content as a borrower decision guide, not a rate ad. AI systems can summarize clear eligibility logic. They are less likely to trust pages that imply every borrower should refinance.

Why Student Loan Refinance GEO Starts With Caveats

Student loan refinance is a high-CPC category because a funded borrower can be valuable. But it is also sensitive: refinancing federal student loans with a private lender can mean giving up federal benefits and protections.

The Consumer Financial Protection Bureau explains that student loan consolidation or refinancing options vary depending on whether the borrower is using a federal Direct Consolidation Loan or a private student loan, and that there are benefits and downsides to each. Federal Student Aid describes federal consolidation and income-driven repayment separately from private refinancing. Useful official references include the CFPB page on consolidating or refinancing student loans , Federal Student Aid's loan consolidation resource, and Federal Student Aid's income-driven repayment information.

That creates a GEO opportunity. Lenders that explain federal-loan caveats clearly can compete on trust, not just APR. The strongest pages make the decision path explicit: who may benefit, who should pause, what to compare, and what assumptions a calculator is using.

The Refinance Decision Matrix helps lenders separate rate-shopping prompts from eligibility, federal-loan tradeoff, cosigner, savings, timing, and trust questions.

The 10 Query Types Student Loan Refinance Teams Should Map

| Query type | Typical borrower | Content that earns trust |

|---|---|---|

| Rate shopping | Borrower comparing APRs | Rate estimate page, fixed vs variable explainer, soft-check guide |

| Eligibility | Borrower unsure if they qualify | Requirements page with approval factors and caveats |

| Federal-loan tradeoff | Borrower with federal loans | Refinance vs federal consolidation guide |

| Private-loan refinance | Borrower already in private loans | Private loan refinance page and savings calculator |

| Cosigner | Borrower with thin credit or low income | Cosigner approval and release guide |

| Credit score | Borrower improving finances | Credit readiness checklist |

| Repayment term | Borrower choosing monthly payment vs total cost | Term comparison calculator |

| Profession scenario | Doctor, nurse, lawyer, teacher, engineer | Career-specific refinance guides with risk notes |

| Lender comparison | Borrower choosing a provider | Lender comparison and checklist page |

| Trust and servicing | Borrower worried about support | Servicer, fee, privacy, and disclosure page |

How To Prioritize Student Loan Refinance AI Search Questions

Score each query by decision impact, approval relevance, savings potential, and caveat risk.

| Factor | High-value signal | Page implication |

|---|---|---|

| Rate intent | Mentions APR, lower rate, fixed, variable, quote | Rate and prequalification page |

| Approval intent | Mentions credit score, income, cosigner, DTI | Eligibility and requirements page |

| Federal risk | Mentions federal loans, PSLF, IDR, forgiveness | Tradeoff page with official references |

| Savings intent | Mentions payment, payoff, calculator, total interest | Calculator and scenario page |

| Comparison intent | Mentions best lender, SoFi alternatives, credit union, bank | Comparison checklist page |

| Timing intent | Mentions when to refinance, rates now, after graduation | Timing and readiness page |

| Trust concern | Mentions safe, legit, hard credit pull, fees, servicer | Trust and disclosure page |

Queries that combine rate intent with federal-loan risk deserve the most careful treatment. They can convert, but they can also push a borrower toward a decision that needs professional or financial review.

100 Student Loan Refinance AI Search Questions

Use this as a prompt library, not a page list.

Rate And APR Questions

- What is a good student loan refinance rate right now?

- How do student loan refinance rates work?

- What is the difference between fixed and variable student loan refinance rates?

- Can I check my student loan refinance rate without hurting my credit?

- Why did I get a higher refinance rate than advertised?

- How does credit score affect student loan refinance rates?

- How does income affect student loan refinance rates?

- Does loan term change my refinance rate?

- Are student loan refinance rates different for graduate loans?

- Should I refinance if rates are higher than my current loan rate?

Eligibility And Approval Questions

- Who qualifies for student loan refinancing?

- What credit score is needed to refinance student loans?

- Can I refinance student loans with low income?

- Can I refinance student loans with a high debt-to-income ratio?

- Do lenders require a degree to refinance student loans?

- Can I refinance if I did not graduate?

- Can international students refinance student loans in the U.S.?

- Can I refinance student loans while unemployed?

- Why was my student loan refinance application denied?

- How can I improve my chances of refinance approval?

Federal Loan Tradeoff Questions

- Should I refinance federal student loans with a private lender?

- What benefits do I lose if I refinance federal student loans?

- Is refinancing the same as federal student loan consolidation?

- Can I use income-driven repayment after refinancing federal loans?

- Can I qualify for PSLF after refinancing federal student loans?

- Should teachers refinance federal student loans?

- Should public service workers refinance student loans?

- Should I refinance federal loans if I may need forbearance?

- What should I compare before refinancing federal loans?

- When does it make sense to refinance only private student loans?

Private Student Loan Questions

- Can I refinance private student loans more than once?

- Is refinancing private student loans worth it?

- Can I refinance private loans from multiple lenders together?

- Can I refinance parent private student loans?

- Can I refinance variable-rate private student loans into fixed loans?

- Can I refinance private loans after my credit improves?

- Can I refinance private student loans with a cosigner?

- Does refinancing private loans reset the repayment term?

- Can refinancing private loans lower my monthly payment?

- What documents are needed to refinance private student loans?

Cosigner Questions

- Do I need a cosigner to refinance student loans?

- Can a cosigner help me get a lower refinance rate?

- What credit score does a cosigner need?

- What risks does a cosigner take on a refinanced student loan?

- Can a cosigner be released after refinancing?

- How long does cosigner release usually take?

- Can I refinance to remove a cosigner from my old loan?

- Can parents cosign student loan refinancing?

- What happens to a cosigner if I miss payments?

- Should I refinance with or without a cosigner?

Savings And Calculator Questions

- How much can student loan refinancing save me?

- How do I calculate student loan refinance savings?

- Should I choose a lower payment or shorter payoff term?

- How does refinancing affect total interest paid?

- Can refinancing student loans help me pay off debt faster?

- Is a 5-year refinance term better than a 10-year term?

- How much should I pay monthly after refinancing?

- Does refinancing reduce principal balance?

- What assumptions should a refinance calculator show?

- When can refinancing cost more over time?

Timing Questions

- When should I refinance student loans?

- Should I refinance student loans before rates change?

- Should I refinance right after graduation?

- Should I refinance during residency?

- Should I refinance after getting a higher-paying job?

- Should I refinance before buying a house?

- Should I refinance while applying for loan forgiveness?

- How often should I check refinance rates?

- Should I wait to refinance until my credit score improves?

- Should I refinance if I plan to pay off loans within two years?

Profession And Scenario Questions

- What are student loan refinance options for doctors?

- What are student loan refinance options for nurses?

- What are student loan refinance options for lawyers?

- What are student loan refinance options for dentists?

- What are student loan refinance options for teachers?

- What are student loan refinance options for engineers?

- Can medical residents refinance student loans?

- Can married borrowers refinance student loans together?

- Can parents refinance Parent PLUS loans?

- Can self-employed borrowers refinance student loans?

Lender Comparison Questions

- How do I compare student loan refinance lenders?

- Which student loan refinance lender is best for high credit scores?

- Which student loan refinance lender is best with a cosigner?

- Should I refinance with a bank, credit union, or fintech lender?

- What fees should I look for when refinancing student loans?

- What is the difference between prequalification and final approval?

- Do student loan refinance lenders charge origination fees?

- How important is customer service when choosing a refinance lender?

- What should I read in a refinance loan agreement?

- How do I compare lender reviews without being misled?

Risk And Trust Questions

- Is student loan refinancing safe?

- Can refinancing student loans hurt my credit?

- What happens if I cannot pay after refinancing?

- Can refinanced student loans be discharged or forgiven?

- What hardship options do private refinance lenders offer?

- What disclosures should a student loan refinance lender provide?

- How do I know if a refinance offer is legitimate?

- What red flags should I watch for in student loan refinance ads?

- Can a lender change my rate after approval?

- What questions should I ask before signing a refinance loan?

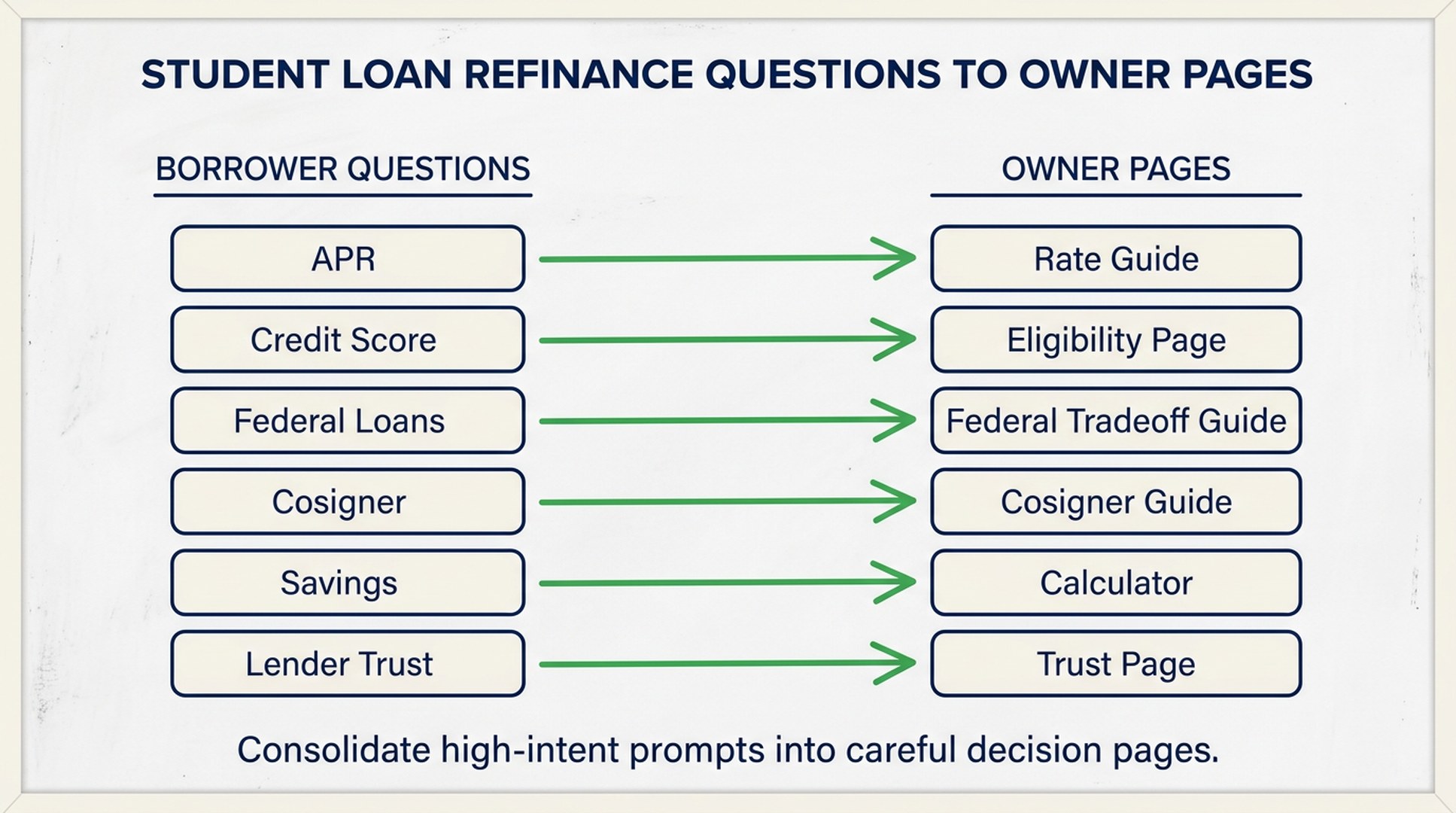

How To Turn These Questions Into Citation-Ready Pages

Most refinance brands should consolidate the 100 questions into 10 to 14 strong owner pages.

| Owner page | Query clusters it should cover | Conversion path |

|---|---|---|

| Student Loan Refinance Rate Guide | 1-10 | Soft rate check or APR education CTA |

| Refinance Eligibility Requirements | 11-20 | Prequalification flow |

| Federal Loan Refinance Tradeoff Guide | 21-30 | Caveat-led decision checklist |

| Private Student Loan Refinance Guide | 31-40 | Refinance quote comparison |

| Cosigner And Cosigner Release Guide | 41-50 | Cosigner-supported application path |

| Refinance Savings Calculator | 51-60 | Calculator to application handoff |

| When To Refinance Guide | 61-70 | Readiness checklist |

| Profession-Specific Refinance Pages | 71-80 | Doctor, nurse, lawyer, dentist, parent borrower pages |

| Lender Comparison Checklist | 81-90 | Comparison table and disclosure page |

| Risk, Hardship, And Trust Guide | 91-100 | Trust page, support policies, disclosures |

Each page should include a direct answer, required caveats, term definitions, eligibility factors, examples with assumptions, disclosure language, and a next step that does not imply guaranteed approval or guaranteed savings.

High-intent refinance prompts should consolidate into durable decision pages instead of near-duplicate rate posts.

The First 20 Questions To Prioritize

| Priority | Question | Best page |

|---|---|---|

| 1 | What is a good student loan refinance rate right now? | Rate Guide |

| 2 | Can I check my student loan refinance rate without hurting my credit? | Soft-Check Page |

| 3 | Who qualifies for student loan refinancing? | Eligibility Requirements |

| 4 | What credit score is needed to refinance student loans? | Credit Readiness Page |

| 5 | Should I refinance federal student loans with a private lender? | Federal Tradeoff Guide |

| 6 | What benefits do I lose if I refinance federal student loans? | Federal Benefit Caveat Page |

| 7 | Is refinancing the same as federal student loan consolidation? | Refinance vs Consolidation Guide |

| 8 | Is refinancing private student loans worth it? | Private Loan Refinance Page |

| 9 | Do I need a cosigner to refinance student loans? | Cosigner Guide |

| 10 | Can a cosigner help me get a lower refinance rate? | Cosigner Rate Page |

| 11 | How much can student loan refinancing save me? | Savings Calculator |

| 12 | Should I choose a lower payment or shorter payoff term? | Term Comparison Page |

| 13 | When should I refinance student loans? | Timing Guide |

| 14 | Should I wait to refinance until my credit score improves? | Refinance Readiness Page |

| 15 | What are student loan refinance options for doctors? | Doctor Refinance Page |

| 16 | What are student loan refinance options for lawyers? | Lawyer Refinance Page |

| 17 | How do I compare student loan refinance lenders? | Lender Comparison Checklist |

| 18 | What fees should I look for when refinancing student loans? | Fee And Disclosure Page |

| 19 | Is student loan refinancing safe? | Risk And Trust Guide |

| 20 | What questions should I ask before signing a refinance loan? | Signing Checklist |

30-Day Execution Plan

Days 1-5: Build The Borrower Question Inventory

- Pull questions from loan applications, chat logs, call transcripts, calculator sessions, ad landing pages, and customer support tickets.

- Tag prompts by rate, approval, federal-loan tradeoff, private-loan refinance, cosigner, savings, timing, profession, lender comparison, and trust.

- Separate federal-loan risk prompts from private-loan shopping prompts.

- Identify official references and competing lender pages that AI systems already cite.

Days 6-10: Publish Rate And Eligibility Assets

- Publish the rate guide, fixed vs variable explanation, and soft credit check page.

- Build the eligibility requirements page with credit, income, degree, loan balance, employment, and debt-to-income factors.

- Add calculator assumptions and disclosure notes.

- Create a comparison block for advertised APR versus personalized quote.

Days 11-15: Build Federal And Private Loan Decision Pages

- Publish the federal-loan tradeoff guide with CFPB and Federal Student Aid references.

- Build a refinance vs federal consolidation guide.

- Create a private student loan refinance page for borrowers who do not risk federal benefits.

- Add a decision checklist that tells uncertain borrowers when to pause.

Days 16-22: Build Cosigner, Savings, And Scenario Pages

- Publish cosigner, cosigner release, and borrower responsibility pages.

- Build a refinance savings calculator page with clearly labeled assumptions.

- Create profession pages for doctors, nurses, lawyers, dentists, teachers, and parent borrowers.

- Add timing content for graduation, residency, credit improvement, job changes, and mortgage planning.

Days 23-30: Test AI Visibility And Improve

- Test the first 20 questions in ChatGPT, Perplexity, Gemini, Google AI Overviews, and Bing Copilot.

- Record brand mentions, cited pages, missing caveats, and rate misinterpretations.

- Improve pages with clearer disclosure language, stronger comparison tables, better examples, and updated internal links.

- Review sensitive financial pages with qualified compliance or legal reviewers before scaling traffic.

Common Mistakes

| Mistake | Why it weakens GEO | Better move |

|---|---|---|

| Leading only with the lowest advertised APR | Borrowers and AI systems need eligibility context | Explain rate ranges, soft checks, and approval factors |

| Treating federal and private loans the same | Federal benefit loss is a major decision risk | Build a dedicated federal-loan tradeoff page |

| Hiding calculator assumptions | AI answers may repeat savings claims without context | Show current balance, rate, term, new rate, term, and total interest assumptions |

| Creating thin profession pages | Repetition weakens trust | Add profession-specific repayment risks and timing factors |

| Overpromising approval | Underwriting depends on borrower facts | Explain prequalification vs final approval |

| Ignoring cosigner risk | Cosigners need clear responsibility language | Publish cosigner and release terms in plain English |

| Skipping hardship policies | Borrowers worry about job loss or income changes | Explain deferment, forbearance, and support options where applicable |

FAQ

Is student loan refinance GEO different from normal SEO?

Yes. Normal SEO often starts with rate keywords and lender comparison pages. Student loan refinance GEO needs to answer borrower decision questions about eligibility, rate estimates, federal-loan tradeoffs, cosigners, savings, timing, and lender trust in a format AI systems can safely summarize.

Should lenders publish content about federal loan risks?

Yes. Avoiding the topic may reduce trust. Explain that refinancing federal student loans with a private lender can affect access to federal repayment plans, forgiveness paths, and other protections. Borrowers should compare those tradeoffs before applying.

Which pages should a refinance lender build first?

Start with a rate guide, eligibility requirements page, federal-loan tradeoff guide, private loan refinance guide, cosigner page, savings calculator, timing guide, lender comparison checklist, and risk/trust page.

Can calculators improve AI Search visibility?

Yes, if the calculator page explains its assumptions in text. AI systems cannot rely on hidden form logic alone. Add examples, definitions, and caveats for payment, total interest, APR, term length, and payoff speed.

How should refinance brands measure AI Search visibility?

Create a fixed prompt set, test it across AI answer platforms, record brand mentions and cited URLs, and check whether answers repeat your caveats correctly. Sensitive prompts should be reviewed for missing federal-loan warnings or exaggerated savings claims.

Auspia Takeaway

Student loan refinance GEO works when it helps borrowers make a careful rate-and-risk decision. The winning content does not just chase "best refinance rate" keywords. It explains qualification, loan type, federal benefit tradeoffs, cosigner responsibility, savings assumptions, timing, and lender trust in a way AI systems can retrieve and summarize accurately.

Author: Simon Vale, 11-Year Search Intent Researcher at Auspia. Simon writes about buyer queries, SERP patterns, intent mapping, and content alignment for high-consideration search categories.