Quick Answer

Financial services and insurance GEO is not about giving personalized financial advice through blog content. It is about making eligibility, fees, policy terms, risk disclosures, coverage limits, claims steps, advisor credentials, and product comparisons easier for AI systems to understand and cite responsibly.

A consumer or business buyer rarely asks only for life insurance, business loan, or retirement account. They ask decision questions:

What type of insurance do I need if I am self-employed?How do I compare term life and whole life insurance?What fees should I check before opening an investment account?Does this policy cover water damage or only sudden leaks?How do I know if a financial advisor is trustworthy?

For regulated categories, GEO should not produce aggressive recommendations, universal advice, or unsupported return claims. The strongest assets are product pages, eligibility guides, fee pages, policy comparison pages, claims guides, risk disclosure pages, advisor profile pages, FAQ pages, and calculators that clearly state assumptions.

This playbook gives financial services and insurance teams 100 AI Search queries to track, a regulated-category prioritization model, a query-to-page map, and a 30-day execution plan.

Important note: this article is about SEO/GEO content strategy, not financial, investment, tax, legal, or insurance advice. Regulated brands should involve compliance, legal, licensed advisors, or product owners before publishing market-facing content.

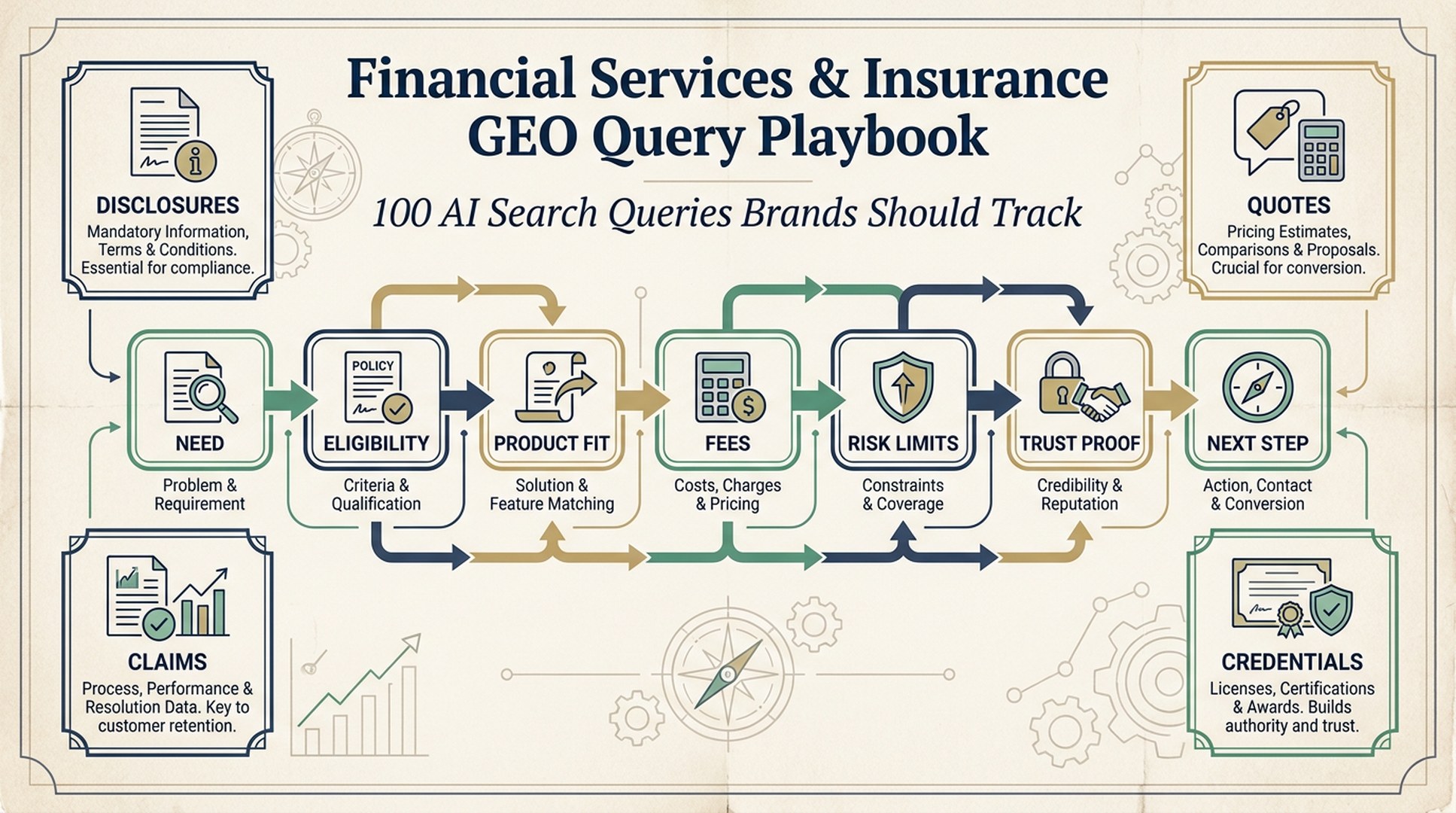

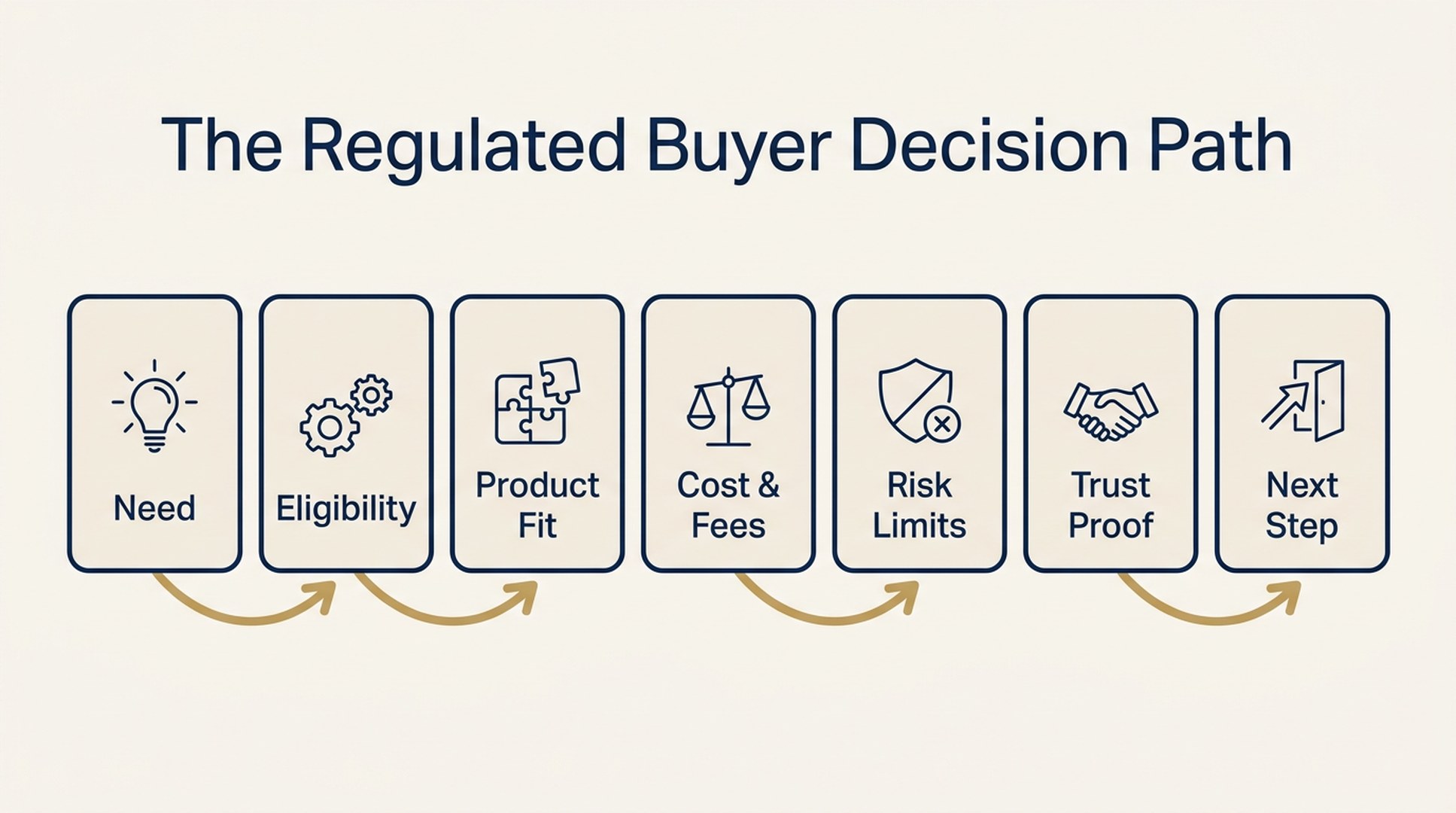

The Regulated Buyer Decision Path

In financial services and insurance, the user journey is shaped by risk. People want to understand whether they qualify, what they might pay, what they are not covered for, what could go wrong, and who they can trust.

A regulated AI Search journey often looks like this:

| Stage | What The User Asks | Page That Should Support The Answer |

|---|---|---|

| Need |

| Need-based guide |

| Eligibility |

| Eligibility page |

| Product Fit |

| Product comparison page |

| Cost / Fee |

| Fee page |

| Risk / Exclusion |

| Exclusions / disclosure page |

| Trust |

| Advisor credentials page |

| Process |

| Claims process page |

| Conversion |

| Quote / consultation page |

This path is different from ecommerce or SaaS. A shopper may tolerate a playful recommendation. A financial or insurance customer needs precise scope, assumptions, limits, eligibility, and risk language.

A useful first step is to check whether the brand appears correctly for priority prompts using an AI Search Visibility Checker , then build a prompt library around inaccurate or missing answers.

Why Financial and Insurance GEO Needs Compliance-Aware Content

The regulated buyer path moves from need and eligibility to product fit, cost, risk limits, trust proof, and a safe next step.

GEO content in regulated categories needs a higher evidence standard. A page that ranks well but implies the wrong coverage, return expectation, eligibility rule, or tax consequence can create legal, compliance, and customer trust problems.

That creates four requirements.

First, assumptions must be visible. If a calculator, quote range, or comparison depends on age, location, credit profile, income, coverage amount, risk tolerance, or policy type, state that clearly.

Second, exclusions and limitations are not optional. AI systems may summarize the most confident text on a page. If your page only highlights benefits and hides exclusions elsewhere, the generated answer may become misleading.

Third, trust signals must be verifiable. Advisor credentials, licenses, registrations, carrier relationships, ratings, disclosures, and review sources should be easy to find.

Fourth, product comparison pages should educate rather than push. A comparison page should explain which option may fit which scenario, what tradeoffs exist, and when the user should seek qualified advice.

The GEO model for regulated financial and insurance content is:

User need -> Eligibility -> Product fit -> Cost and fees -> Risk limits -> Trust proof -> Next step

The 10 Query Types Financial and Insurance Brands Should Map

Classify queries before writing pages. This prevents teams from publishing repetitive “best insurance” or “best financial product” pages without enough disclosure.

| Query Type | What The User Wants | Best Content Asset |

|---|---|---|

| Need | Understand what product, policy, account, or service may fit a situation | Need-based guide |

| Eligibility | Know whether they may qualify or what factors matter | Eligibility page, FAQ |

| Product Fit | Compare account types, policies, coverage, loan options, or advisory models | Product comparison page |

| Cost / Fee | Understand premiums, fees, rates, deductibles, commissions, or total cost | Fee page, pricing guide |

| Risk / Exclusion | Understand what is not covered, what can go wrong, or what assumptions apply | Disclosure / exclusions page |

| Quote / Estimate | Understand quote inputs, rate factors, and calculator assumptions | Quote page, calculator guide |

| Claims / Process | Understand application, underwriting, claims, transfer, or cancellation steps | Process page |

| Trust / Credentials | Verify advisor, broker, carrier, lender, or platform credibility | Credentials page, About page |

| Comparison / Alternative | Compare brands, policy types, providers, or product structures | Comparison page |

| Scenario / Life Stage | Match product needs to business type, family stage, income, property, or risk profile | Scenario guide |

Every high-value query cluster should have one owner page. If eligibility is answered differently on a blog post, product page, and FAQ, AI systems may summarize the wrong version.

How To Prioritize Financial and Insurance GEO Queries

Use a regulated-category scoring model:

Priority = Decision Intent + Revenue Fit + Eligibility Clarity + Evidence Strength + AI Answer Probability - Compliance Risk - Competition Difficulty

| Factor | How To Evaluate It |

|---|---|

| Decision Intent | Is the user comparing products, checking eligibility, requesting a quote, or preparing to speak with an advisor? |

| Revenue Fit | Does the query match a product or service the brand actually wants to sell responsibly? |

| Eligibility Clarity | Can the answer state clear factors without overpromising approval, coverage, or returns? |

| Evidence Strength | Do you have product documents, fee schedules, policy language, disclosures, advisor credentials, calculators, or claims data? |

| AI Answer Probability | Is the query likely to trigger a summarized comparison, explanation, or recommendation? |

| Compliance Risk | Could the answer imply personalized advice, guaranteed returns, guaranteed approval, or misleading coverage? |

| Competition Difficulty | Are government sites, large carriers, banks, brokerages, review sites, or aggregators dominating the topic? |

Start with queries that help users understand fit, cost, eligibility, process, and risk. Avoid starting with aggressive “best product” content unless the page has strong evidence, disclaimers, and a clear methodology.

100 Financial Services and Insurance GEO Query Examples

Use these prompts as a starting library. Adapt them by jurisdiction, product type, disclosure requirements, and compliance review.

Need Queries

- What type of insurance does a freelancer need?

- What insurance should a small business consider?

- What financial accounts should a new business owner understand?

- What should first-time homebuyers know about mortgage options?

- What insurance should renters consider?

- What coverage should landlords consider?

- What should parents consider before buying life insurance?

- What should self-employed people know about retirement accounts?

- What should a startup know before choosing business banking?

- What should a family consider before choosing health insurance?

Eligibility Queries

- Can I qualify for a business loan if I am self-employed?

- Can I get life insurance with a medical condition?

- Can I get car insurance after an accident?

- Can I open a retirement account if I am self-employed?

- What affects mortgage eligibility?

- What affects small business loan approval?

- What affects life insurance eligibility?

- What affects health insurance plan eligibility?

- What affects insurance underwriting?

- What documents are needed to apply for a loan?

Product Fit Queries

- Term life vs whole life insurance: what is the difference?

- HMO vs PPO health insurance: what is the difference?

- Fixed-rate mortgage vs adjustable-rate mortgage

- Personal loan vs credit card for a large purchase

- Business line of credit vs business loan

- Traditional IRA vs Roth IRA

- High-deductible health plan vs low-deductible plan

- Comprehensive vs collision auto insurance

- General liability vs professional liability insurance

- Independent advisor vs robo-advisor

Cost / Fee Queries

- How much does term life insurance usually cost?

- What affects car insurance premiums?

- What affects homeowners insurance premiums?

- What fees should I check before opening an investment account?

- What does an expense ratio mean?

- What fees do financial advisors charge?

- What affects mortgage closing costs?

- What affects business loan interest rates?

- What is an insurance deductible?

- What is the difference between premium and deductible?

Risk / Exclusion Queries

- What does homeowners insurance usually not cover?

- Does renters insurance cover water damage?

- What does travel insurance usually exclude?

- What are common exclusions in business insurance?

- What risks should I understand before investing?

- What does FDIC insurance cover and not cover?

- What happens if I miss an insurance premium payment?

- What happens if a claim is denied?

- What should I check before buying investment products online?

- What should I check before signing a loan agreement?

Quote / Estimate Queries

- What information is needed for an insurance quote?

- Why do insurance quotes vary between companies?

- How accurate are online insurance quotes?

- What information is needed for a mortgage estimate?

- What information is needed for a business loan quote?

- How do insurers calculate premiums?

- How do lenders calculate loan rates?

- What assumptions should a retirement calculator disclose?

- What assumptions should an insurance calculator disclose?

- Why did my quote change after underwriting?

Claims / Process Queries

- How does the insurance claims process work?

- What should I do after a car accident before filing a claim?

- What documents are needed for a homeowners insurance claim?

- How long does an insurance claim usually take?

- What happens during life insurance underwriting?

- What happens after submitting a mortgage application?

- What happens after applying for a business loan?

- How do I cancel an insurance policy?

- How do I switch insurance providers?

- How do I transfer an investment account?

Trust / Credentials Queries

- How do I know if a financial advisor is trustworthy?

- How do I verify an insurance agent license?

- How do I verify a mortgage broker license?

- What credentials should a financial advisor have?

- What should I look for in an insurance broker?

- Are online reviews reliable for financial advisors?

- What should a financial services website disclose?

- What makes an insurance company trustworthy?

- What should I ask before choosing a financial advisor?

- How do I compare insurance company ratings?

Comparison / Alternative Queries

- Best insurance provider for freelancers

- Best business insurance for small companies

- Best bank account for a small business

- Best retirement account for self-employed workers

- Best health insurance option for families

- Best auto insurance for new drivers

- Best mortgage option for first-time buyers

- Best financial advisor model for beginners

- Insurance broker vs direct insurance company

- Online lender vs traditional bank loan

Scenario / Life Stage Queries

- What insurance should new parents consider?

- What financial products should freelancers understand?

- What should retirees know before changing insurance plans?

- What should small business owners know about liability coverage?

- What should landlords know about insurance?

- What should homeowners know before refinancing?

- What should young professionals know about retirement savings?

- What should families compare during open enrollment?

- What should startups check before choosing business insurance?

- What should gig workers know about income protection?

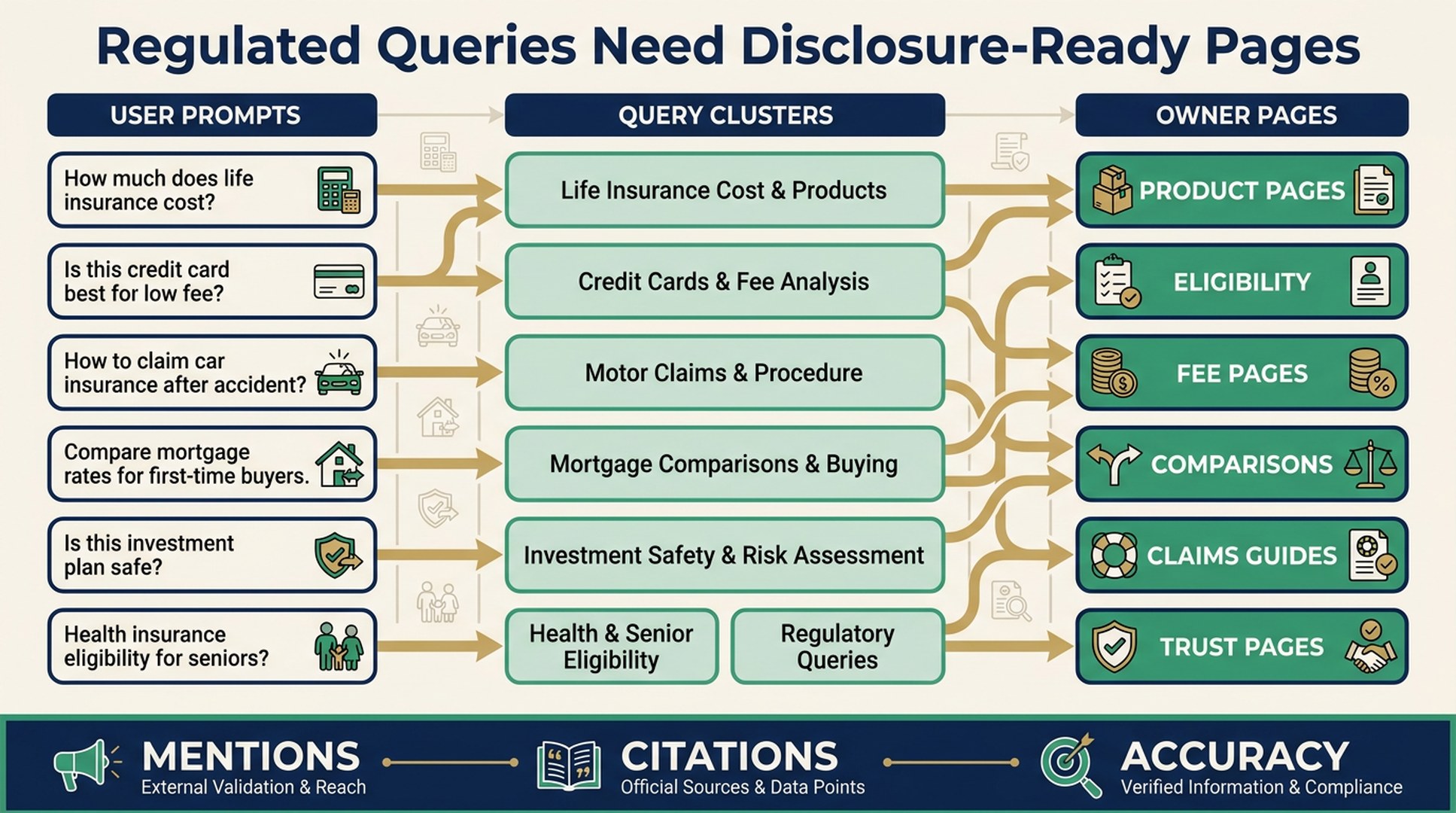

How To Turn Financial and Insurance Queries Into Citation-Ready Pages

A regulated query library should become a trust and disclosure architecture. The strongest pages are product pages, comparison pages, fee pages, eligibility pages, policy pages, claim guides, and advisor profile pages.

| Query Cluster | Owner Page | Page Type | Required Proof |

|---|---|---|---|

| Need prompts | Need-based guide | Educational guide | Product scope, scenario fit, no-advice disclaimer |

| Eligibility prompts | Eligibility page | FAQ / product guide | Qualification factors, documents, caveats, update date |

| Product-fit prompts | Product comparison page | Comparison page | Tradeoffs, assumptions, who each option may fit |

| Cost and fee prompts | Fee page | Pricing / fee guide | Fees, premiums, deductibles, commissions, examples |

| Risk and exclusion prompts | Disclosure page | Risk / exclusions page | Exclusions, limitations, policy references, warnings |

| Quote prompts | Quote guide | Quote / calculator page | Inputs, assumptions, underwriting caveats |

| Process prompts | Application / claims guide | Process page | Steps, documents, timeline ranges, contact path |

| Trust prompts | Credentials page | Advisor / company trust page | Licenses, registrations, ratings, disclosures |

| Comparison prompts | Provider / product comparison | Comparison page | Methodology, scope, caveats, non-guarantee language |

| Scenario prompts | Life-stage guide | Scenario page | Segment-specific considerations, CTA, disclaimers |

A strong financial or insurance GEO page should answer the user's decision question while making limits clear. The most citation-ready page is often not the most promotional page; it is the page that states facts, assumptions, risks, and next steps in plain language.

For technical readiness, regulated brands should make sure product pages, policy pages, disclosure pages, and advisor profiles are crawlable and indexable. A quick Website SEO Score Checker can help surface basic technical issues before content teams rewrite regulated pages.

Each high-risk query cluster should resolve to one owner page so AI systems do not piece together conflicting answers from scattered content.

The First 20 Queries To Prioritize

If a financial services or insurance brand is starting from scratch, these 20 prompts usually create a practical first backlog.

| Priority | Query | Why It Matters | Likely Owner Page |

|---|---|---|---|

| 1 | What type of insurance does a freelancer need? | Need-based product fit | Scenario guide |

| 2 | What insurance should a small business consider? | High commercial fit | Business insurance guide |

| 3 | Term life vs whole life insurance | High comparison intent | Product comparison page |

| 4 | HMO vs PPO health insurance | Common decision query | Health plan comparison |

| 5 | What affects insurance premiums? | Cost expectation | Pricing guide |

| 6 | What fees should I check before opening an investment account? | Trust and cost query | Fee page |

| 7 | What does homeowners insurance usually not cover? | Risk and exclusion query | Exclusions page |

| 8 | What happens if a claim is denied? | High anxiety process query | Claims FAQ |

| 9 | What information is needed for an insurance quote? | Quote conversion | Quote page |

| 10 | Why did my quote change after underwriting? | Accuracy and trust | Underwriting FAQ |

| 11 | How does the insurance claims process work? | Process clarity | Claims guide |

| 12 | What documents are needed for a homeowners insurance claim? | Practical action | Claims checklist |

| 13 | How do I know if a financial advisor is trustworthy? | Trust validation | Advisor credentials page |

| 14 | How do I verify an insurance agent license? | Credential validation | License guide |

| 15 | What should a financial services website disclose? | Compliance and trust | Disclosure page |

| 16 | Insurance broker vs direct insurance company | Provider comparison | Broker comparison page |

| 17 | Online lender vs traditional bank loan | Product/provider comparison | Lending comparison page |

| 18 | What should families compare during open enrollment? | Seasonal demand | Open enrollment guide |

| 19 | What should startups check before choosing business insurance? | Segment-specific fit | Startup insurance guide |

| 20 | What should I check before signing a loan agreement? | High-risk decision | Loan agreement checklist |

These prompts are useful because they can be answered with educational, disclosure-aware content rather than unsupported personalized advice.

30-Day Execution Plan

| Timeframe | Action | Output |

|---|---|---|

| Days 1-3 | Build the finance and insurance AI Search query library and classify by product, risk, eligibility, and page owner | 100-query prompt library |

| Days 4-7 | Score prompts by decision intent, revenue fit, eligibility clarity, evidence, AI answer probability, compliance risk, and difficulty | First 20 prompt backlog |

| Days 8-14 | Map prompts to product pages, fee pages, eligibility pages, comparison pages, quote pages, claims guides, and trust pages | Query-to-page map |

| Days 15-21 | Rewrite priority pages with direct answers, assumptions, exclusions, disclosures, credentials, and clear next steps | Updated citation-ready pages |

| Days 22-30 | Test prompts across AI answer surfaces and record brand mentions, cited URLs, competitors, and inaccurate product facts | Regulated AI visibility tracker |

A small insurance agency can start with five assets: one need-based guide, one product comparison page, one quote FAQ, one claims guide, and one license/trust page. A larger financial brand should add product pages, calculators, disclosure pages, advisor profiles, and scenario hubs.

Common Mistakes

Financial services and insurance GEO fails when teams chase rankings without managing risk and accuracy.

Avoid these mistakes:

- Publishing universal recommendations. Explain scenarios and tradeoffs instead of telling every user what to buy.

- Hiding exclusions and assumptions. AI systems may summarize benefits without limits if limits are hard to find.

- Using calculators without assumptions. State inputs, limitations, update date, and whether results are estimates.

- Overclaiming savings, returns, or approval odds. Avoid unsupported promises.

- Treating disclosures as separate from content. Disclosures and risk language should be visible near relevant claims.

- Ignoring advisor and broker trust. Licenses, credentials, registrations, and review sources should be easy to verify.

- Measuring only organic rankings. Track AI mentions, cited URLs, competitor inclusion, and inaccurate product descriptions.

FAQ

What is financial services GEO?

Financial services GEO is the process of making financial, insurance, lending, advisory, policy, fee, eligibility, and disclosure pages easier for AI answer systems to understand, summarize, and cite accurately.

Is financial GEO the same as financial SEO?

No. Financial SEO focuses on search visibility, rankings, technical health, content quality, and conversions. Financial GEO builds on that foundation but focuses on how AI systems summarize products, explain tradeoffs, mention brands, and handle risk-sensitive queries.

Should financial brands publish 100 blog posts for 100 AI queries?

No. A regulated query library should become a page map. Many questions should be answered by product pages, eligibility pages, fee pages, comparison pages, quote pages, claims guides, disclosure pages, and advisor profiles.

Which finance and insurance queries should teams start with?

Start with questions about eligibility, fees, policy fit, product comparisons, exclusions, claims process, quotes, advisor credentials, and scenario-specific needs. These queries influence decisions and can be answered with evidence and disclosures.

How can regulated brands avoid risky GEO content?

Use compliance review, clear assumptions, disclaimers where appropriate, visible exclusions, no return or approval guarantees, accurate fee language, and advisor or product-owner review. The goal is to clarify decisions, not provide personalized advice on a public page.

How should finance and insurance teams measure GEO performance?

Track a stable prompt set across AI answer surfaces. Record whether the brand appears, which URLs are cited, which competitors appear, whether product facts are accurate, and whether AI answers omit important eligibility, risk, or fee information.

Auspia Takeaway

Financial services and insurance GEO is about responsible clarity. AI systems need eligibility factors, product scope, fee details, exclusions, claims steps, trust signals, and next actions before they can summarize a brand safely.

Start with risk-aware prompts. Map the first 20 queries to pages that already influence quotes, applications, advisor conversations, or policy selection. The strongest regulated GEO content is not the loudest; it is the clearest, most accurate, and easiest to verify.

Author: Grace Miller, AI Search Risk Analyst Tracking 200+ Policy Shifts at Auspia. Grace writes about platform rules, content risk, policy-aware optimization, and safe AI visibility programs for regulated teams.