Quick Answer

Business loan GEO is not about repeating phrases like business loan, small business financing, or fast funding across every page. It is about answering the questions a business owner asks before they trust a lender with cash flow, repayment obligations, collateral, credit checks, and timing.

For lenders, fintech teams, brokers, and SMB finance platforms, the highest-value AI Search prompts usually sit in six zones:

| Buyer question | Best owner page | Proof AI systems can extract |

|---|---|---|

| Can I qualify? | Eligibility guide | Revenue, time in business, credit, industry, documentation |

| What will it cost? | Rate and APR explainer | APR, factor rate, fees, term length, repayment examples |

| How fast can I get funded? | Funding timeline page | Steps, documents, verification, realistic delays |

| What loan type fits my situation? | Product fit matrix | Term loan, line of credit, SBA, equipment, invoice financing |

| What are the risks? | Repayment and cash-flow guide | Payment cadence, penalties, refinancing limits |

| Which lender should I compare? | Lender comparison page | Fit criteria, underwriting model, service model, tradeoffs |

This playbook gives business loan marketers a practical framework, 100 AI Search query examples, a page architecture, and a 30-day execution plan.

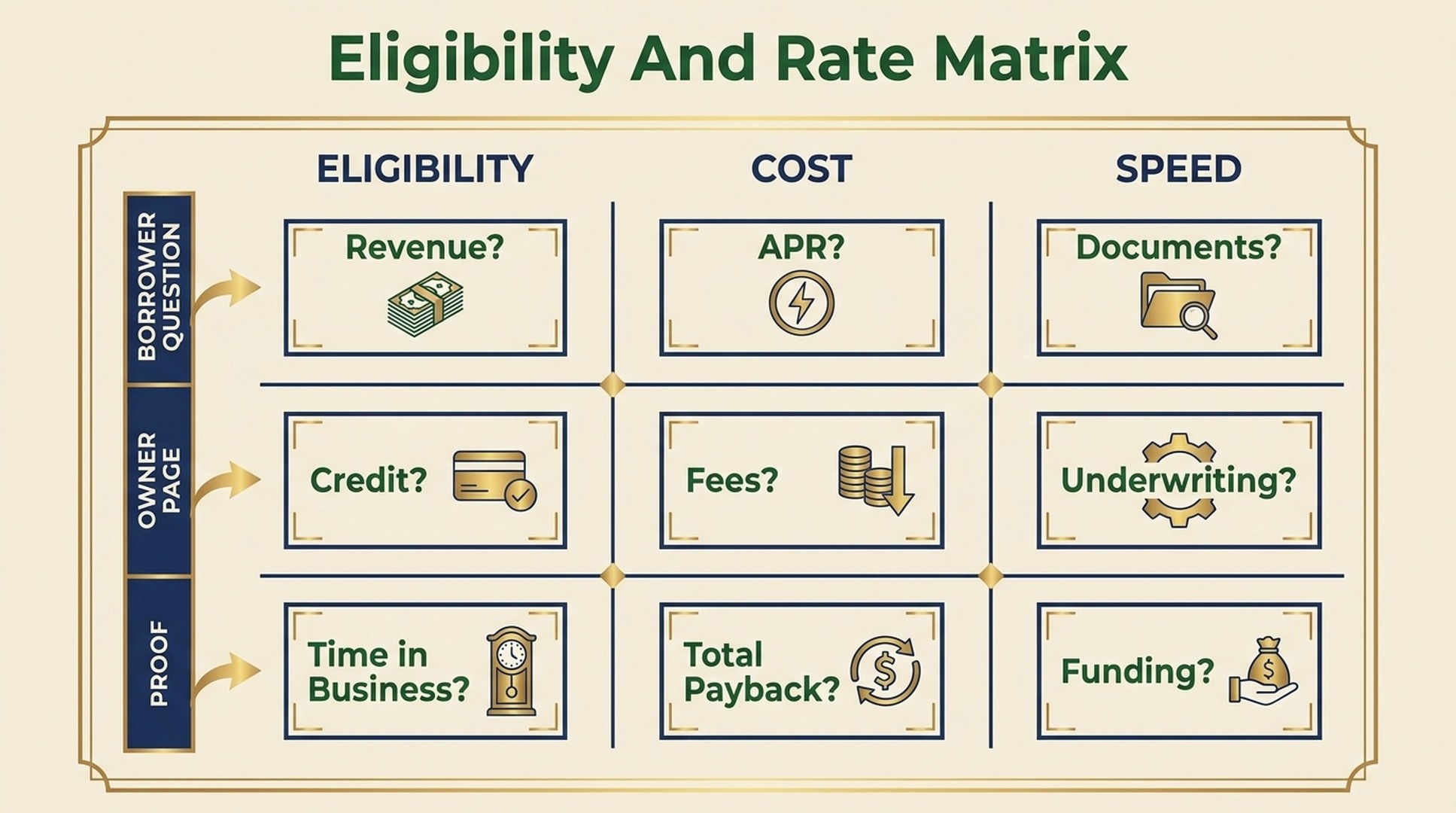

The Eligibility And Rate Matrix

A business loan decision is usually shaped by two forces: eligibility and cost. Borrowers first ask, "Can I get approved?" Then they ask, "Will this financing hurt or help my cash flow?"

The Eligibility And Rate Matrix helps teams avoid generic lending content by mapping every query to a real underwriting or repayment concern.

| Matrix zone | What the borrower needs to understand | Content job |

|---|---|---|

| Eligibility | Whether the business can qualify | Explain revenue, credit, operating history, industry, and documents |

| Loan fit | Which financing product matches the use case | Compare term loans, lines of credit, SBA loans, equipment loans, invoice financing, and MCA alternatives |

| Cost | What the money really costs | Show APR, fees, factor rates, repayment examples, and total payback |

| Speed | How quickly funds can arrive | Separate prequalification, underwriting, approval, and disbursement |

| Risk | What can go wrong after funding | Explain repayment pressure, collateral, guarantees, defaults, and renewal traps |

| Comparison | How to choose a lender | Provide fit criteria instead of vague "best lender" claims |

Auspia's recommendation: build pages that help a borrower choose safely, not just apply quickly. AI answer systems are more likely to reuse a page that clearly explains tradeoffs than one that only promises fast capital.

Why Business Loan GEO Starts With Decision Friction

Business lending has high commercial value because the decision is urgent and expensive. A restaurant owner may need cash before payroll. A contractor may need a line of credit before buying materials. An ecommerce brand may need inventory financing before a seasonal spike. A founder may compare bank loans, online lenders, SBA loans, credit lines, and merchant cash advances in one session.

AI Search makes that journey more conversational. Instead of typing one keyword, borrowers ask layered questions:

- "Can I get a business loan with 580 credit and six months of revenue?"

- "Is a line of credit better than a term loan for working capital?"

- "What documents do lenders ask for before approval?"

- "How do factor rates compare with APR?"

- "What is the safest fast funding option for a small business?"

Those prompts include eligibility, product fit, cost, speed, and risk. A lender that only has a generic application page gives AI systems very little to cite. A lender with clear owner pages can become a better source for the answer.

The Eligibility And Rate Matrix keeps business loan GEO focused on qualification, cost, speed, and proof instead of generic loan keywords.

The 10 Query Types Business Loan Teams Should Map

| Query type | Typical user | Content that earns trust |

|---|---|---|

| Eligibility | Business owner, finance manager | Qualification guide, prequalification FAQ |

| Rate and cost | Owner, CFO, bookkeeper | APR explainer, fee table, repayment examples |

| Product fit | Founder, operator | Loan type matrix and use-case pages |

| Funding speed | Urgent borrower | Timeline page and document checklist |

| Documentation | Office manager, bookkeeper | Application checklist and document examples |

| Credit and collateral | Owner with risk concerns | Personal guarantee, collateral, credit impact guide |

| Comparison | Evaluating borrower | Lender comparison and alternatives pages |

| Industry scenario | Restaurant, contractor, ecommerce, medical practice | Vertical-specific financing guides |

| Repayment risk | Cautious borrower | Cash-flow calculator content, default and renewal guidance |

| Alternatives | Borrower comparing options | SBA, line of credit, invoice financing, equipment financing, MCA alternatives |

How To Prioritize Business Loan GEO Queries

Score each query before assigning it to content.

| Factor | High-value signal | Page implication |

|---|---|---|

| Qualification pressure | Mentions approval, credit score, revenue, time in business | Eligibility guide or prequalification page |

| Cost sensitivity | Mentions APR, fee, payment, factor rate, total payback | Rate and repayment explainer |

| Funding urgency | Mentions fast, same day, emergency, payroll, inventory | Funding timeline and document checklist |

| Product uncertainty | Mentions term loan, line of credit, SBA, equipment, invoice | Product fit matrix |

| Risk awareness | Mentions collateral, personal guarantee, default, cash flow | Risk and repayment guide |

| Commercial fit | Mentions lender, compare, best, alternative, application | Comparison or conversion page |

Queries with both cost sensitivity and commercial fit deserve careful attention. They are not just traffic prompts. They influence whether a borrower trusts the lender enough to apply.

100 Business Loan AI Search Query Examples

Use these as a prompt library, not as 100 separate page ideas.

Eligibility Queries

- What are the basic requirements for a small business loan?

- Can I get a business loan with bad credit?

- What credit score do I need for a business loan?

- How much monthly revenue do lenders require for a business loan?

- Can a new business qualify for financing?

- How long do I need to be in business before applying for a loan?

- What industries have a harder time getting business loans?

- Can a sole proprietor get a business loan?

- Can I prequalify for a business loan without hurting my credit?

- Why was my business loan application denied?

Rate And Cost Queries

- What is a good interest rate for a small business loan?

- How do business loan APR and interest rate differ?

- What fees should I expect with a business loan?

- How do factor rates work in small business financing?

- How do I calculate the total cost of a business loan?

- What makes one business loan more expensive than another?

- Are fast business loans usually more expensive?

- How does repayment term affect business loan cost?

- What is the difference between simple interest and APR for business loans?

- How can I compare business loan offers fairly?

Product Fit Queries

- Is a term loan or line of credit better for working capital?

- What type of loan is best for buying business equipment?

- Should a small business use invoice financing or a line of credit?

- What is the difference between SBA loans and online business loans?

- Which financing option is best for inventory purchases?

- What loan type fits a seasonal business?

- Is a merchant cash advance the same as a business loan?

- When should a business use equipment financing?

- What is the safest financing option for short-term cash flow?

- How do I choose the right business loan product?

Funding Speed Queries

- How fast can a small business loan be funded?

- Can I get business funding the same day?

- What slows down business loan approval?

- How long does underwriting take for a business loan?

- What documents should I prepare for fast funding?

- Why do bank business loans take longer than online loans?

- Can I get emergency business funding for payroll?

- How quickly can a line of credit be approved?

- What is the fastest safe way to get business capital?

- How can I avoid delays in a business loan application?

Documentation Queries

- What documents are needed for a business loan application?

- Do lenders require business bank statements?

- How many months of revenue statements do I need for a business loan?

- Do I need tax returns for a business loan?

- What financial statements do lenders review?

- Do online lenders verify bank account activity?

- What documents prove business ownership?

- How should I prepare my books before applying for financing?

- Do lenders require a business plan for a loan?

- What documents are needed for SBA loan prequalification?

Credit And Collateral Queries

- Does a business loan require a personal guarantee?

- Can I get a business loan without collateral?

- Will applying for a business loan affect my personal credit?

- Do business lenders check personal or business credit?

- What happens if I default on a business loan?

- Can I get financing after a previous loan default?

- How do secured and unsecured business loans differ?

- What assets can be used as collateral for a business loan?

- Can a business loan build business credit?

- How do lenders evaluate cash flow and credit risk?

Comparison Queries

- What is the best business loan for a small company?

- How should I compare online business lenders?

- What questions should I ask before choosing a business lender?

- Are online business loans better than bank loans?

- How do lender reviews matter when choosing a business loan?

- What should I look for in a business loan offer?

- How do brokers compare with direct lenders?

- What are red flags in small business financing offers?

- How do I compare repayment schedules across lenders?

- What makes a business loan provider trustworthy?

Industry Scenario Queries

- What is the best business loan for a restaurant?

- How can contractors finance materials before getting paid?

- What funding options work for ecommerce inventory?

- Can a medical practice get financing for equipment?

- What business loan fits a trucking company?

- How can a salon or spa finance expansion?

- What funding options work for franchise owners?

- Can a construction company get a line of credit?

- What business financing works for seasonal retail?

- How should a professional services firm finance growth?

Repayment Risk Queries

- How much business loan payment can my company afford?

- How do daily or weekly repayments affect cash flow?

- What happens if business revenue drops after taking a loan?

- Can I repay a business loan early without penalties?

- How do renewal offers affect total borrowing cost?

- What are the risks of stacking business loans?

- How should I model repayment before accepting a loan?

- What cash-flow metrics should I check before borrowing?

- How can a business avoid debt traps?

- When should a business not take a loan?

Alternative Financing Queries

- What are alternatives to a business loan?

- Is invoice factoring better than a business loan?

- Should I use a business credit card or line of credit?

- Is revenue-based financing a good option for small businesses?

- How does equipment leasing compare with equipment financing?

- What is the difference between a merchant cash advance and a loan?

- Is an SBA loan worth the longer approval process?

- What financing options work without strong personal credit?

- How should I compare debt financing and equity financing?

- What is the safest way to finance business growth?

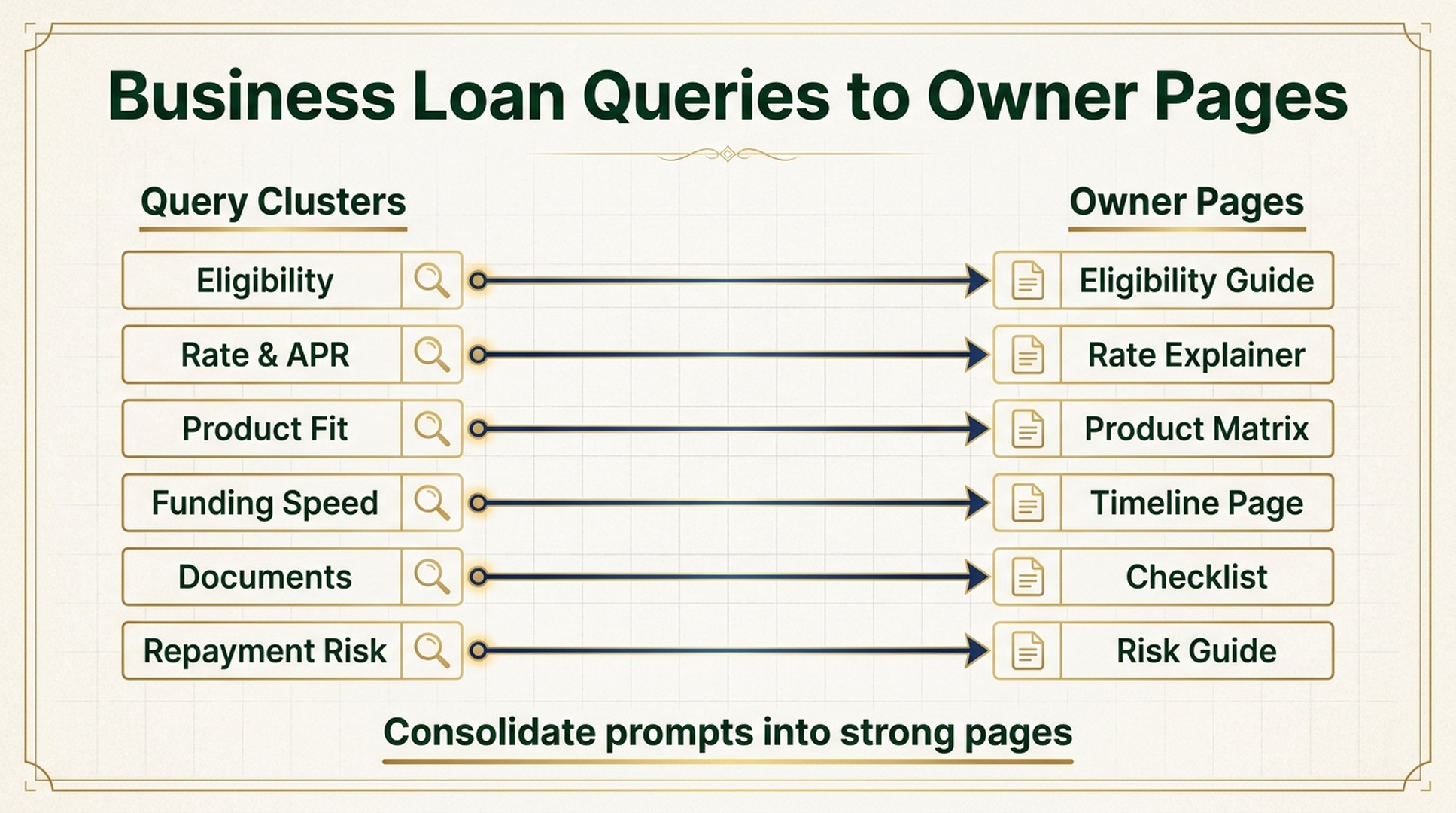

How To Turn Business Loan Queries Into Citation-Ready Pages

Do not turn this prompt library into a thin programmatic SEO project. Build durable owner pages that can answer many prompts at once.

| Owner page | Query clusters it should cover | Conversion path |

|---|---|---|

| Business Loan Eligibility Guide | 1-10, 51-60 | Prequalification or application |

| Rate, APR, And Fee Explainer | 11-20, 81-90 | Cost calculator or consultation |

| Loan Type Fit Matrix | 21-30, 91-100 | Product selector |

| Funding Timeline And Document Checklist | 31-50 | Fast funding application |

| Lender Comparison Guide | 61-70 | Offer review or demo |

| Industry Financing Guides | 71-80 | Vertical landing pages |

| Repayment Risk Guide | 81-90 | Responsible borrowing checklist |

A strong page should include a direct answer, eligibility ranges, examples, document checklists, cost tables, risk notes, and clear calls to action. It should also avoid guaranteeing approval, hiding fees, or implying that fast funding is always the safest choice.

Business loan prompt clusters should consolidate into strong owner pages that help borrowers compare options safely.

The First 20 Queries To Prioritize

| Priority | Query | Best owner page |

|---|---|---|

| 1 | What are the basic requirements for a small business loan? | Eligibility Guide |

| 2 | Can I get a business loan with bad credit? | Credit Guide |

| 3 | What is a good interest rate for a small business loan? | Rate Explainer |

| 4 | How do business loan APR and interest rate differ? | APR Guide |

| 5 | Is a term loan or line of credit better for working capital? | Product Fit Matrix |

| 6 | What type of loan is best for buying business equipment? | Equipment Financing Page |

| 7 | How fast can a small business loan be funded? | Funding Timeline |

| 8 | What documents are needed for a business loan application? | Document Checklist |

| 9 | Does a business loan require a personal guarantee? | Risk Guide |

| 10 | Can I get a business loan without collateral? | Collateral Guide |

| 11 | What is the best business loan for a small company? | Comparison Page |

| 12 | What are red flags in small business financing offers? | Trust Guide |

| 13 | What is the best business loan for a restaurant? | Restaurant Financing Guide |

| 14 | How can contractors finance materials before getting paid? | Contractor Financing Guide |

| 15 | How much business loan payment can my company afford? | Repayment Guide |

| 16 | What are the risks of stacking business loans? | Debt Risk Guide |

| 17 | What are alternatives to a business loan? | Alternatives Guide |

| 18 | Is an SBA loan worth the longer approval process? | SBA Comparison |

| 19 | What is the fastest safe way to get business capital? | Speed And Safety Page |

| 20 | How should I compare business loan offers fairly? | Offer Comparison Guide |

30-Day Execution Plan

Days 1-5: Build The Borrower Question Set

- Pull questions from sales calls, chat logs, loan officers, rejected applications, and broker notes.

- Tag each question by eligibility, cost, product fit, speed, risk, and industry.

- Separate education prompts from application-intent prompts.

- Identify queries where competitors or generic finance sites currently own the answer.

Days 6-10: Build Eligibility And Cost Assets

- Publish the eligibility guide and rate/APR explainer first.

- Add examples with clear assumptions, not vague promises.

- Explain what prequalification means and what it does not guarantee.

- Link to calculators, application pages, and responsible borrowing content.

Days 11-15: Build Product Fit And Documentation Pages

- Create the loan type matrix.

- Add funding timeline and document checklist pages.

- Show which documents commonly delay approval.

- Explain differences between bank, SBA, online lender, broker, and alternative financing workflows.

Days 16-22: Build Comparison And Scenario Pages

- Publish lender comparison guidance.

- Add vertical guides for restaurants, contractors, ecommerce, professional services, and healthcare practices.

- Make each scenario specific: cash-flow timing, collateral, documentation, revenue seasonality, and repayment cadence.

Days 23-30: Test AI Visibility And Improve

- Run the top 20 prompts in ChatGPT, Perplexity, Gemini, Google AI Overviews, and Bing Copilot.

- Track whether the brand appears, which pages are cited, and whether answers mention competitors.

- Improve pages with missing examples, unclear fee language, weak comparison criteria, or thin FAQs.

- Add internal links from guides to conversion pages without making the content feel like a sales script.

Common Mistakes

| Mistake | Why it weakens GEO | Better move |

|---|---|---|

| Treating every loan query as the same intent | Borrowers ask about approval, cost, speed, risk, and fit separately | Segment prompts by decision friction |

| Hiding cost language | AI answers need clear definitions and comparisons | Explain APR, fees, factor rates, and total payback |

| Promising approval or instant funding | Lending decisions depend on underwriting and verification | Use realistic conditions and caveats |

| Creating thin pages for every industry | Repetitive content is weak for readers and AI systems | Build strong scenario pages for high-value industries first |

| Ignoring repayment risk | Borrowers worry about cash flow after funding | Include repayment examples and risk guidance |

| Overusing "best lender" claims | Generic rankings are hard to trust | Explain fit criteria and tradeoffs |

| Sending every query to an application page | Not every borrower is ready to apply | Use guides, calculators, checklists, and comparison pages |

FAQ

Is GEO for business loan providers different from traditional SEO?

Yes. Traditional SEO often starts with keyword volume and ranking pages. GEO also asks whether AI answer systems can extract a clear answer from your content when a borrower asks a multi-part financing question. That requires tables, examples, definitions, caveats, and decision frameworks.

Should a lender create one page for every business loan query?

No. Most business loan queries should map to a smaller number of strong owner pages. Thin pages that repeat the same approval and funding language are less useful than durable guides that cover eligibility, cost, documents, product fit, and risk in detail.

Which business loan pages should be built first?

Start with eligibility, rate/APR, loan type fit, document checklist, funding timeline, lender comparison, and repayment risk pages. These cover the questions that most often block a borrower from applying.

How can lenders avoid risky claims in GEO content?

Use conditional language. Explain what factors affect approval and cost, avoid guaranteed approval claims, disclose that terms vary by borrower and lender, and show examples with assumptions. Responsible content can still convert well because it builds trust.

How should a lender measure AI Search visibility?

Create a fixed prompt set, test it across AI answer platforms, record whether the brand appears, capture cited sources, and review answer quality. The first 20 queries in this article are a practical starting set.

Auspia Takeaway

Business loan GEO works when content respects the borrower's real decision path: qualification, cost, product fit, speed, documents, risk, and alternatives. If your pages only push fast applications, AI systems have little useful context to cite. If your pages explain tradeoffs clearly and connect borrowers to the right next step, they can support both AI visibility and higher-quality leads.

Author: Leah Foster, Conversion SEO Strategist for 400+ Landing Pages at Auspia. Leah writes about landing pages, conversion paths, and content-to-application journeys for search and AI visibility.